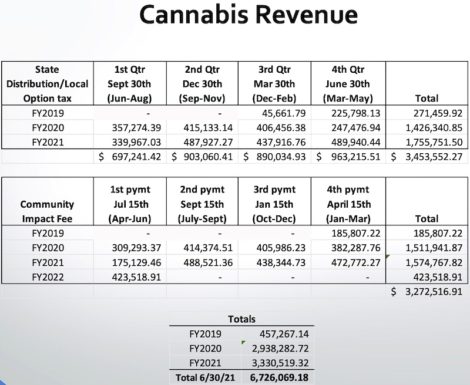

GREAT BARRINGTON — Since its first recreational marijuana stores opened in January 2019, the town of Great Barrington has taken in a total of more than $6.7 million in cannabis-related revenues.

The numbers were confirmed to the selectboard by town Finance Director Susan Carmel in a discussion Monday night. Click here to view Carmel’s presentation, which includes a per-quarter breakdown by individual retailers.

The bulk of the revenues come from so-called local-option taxes on meals, hotel rooms, and cannabis sales. In 2010, the town adopted such taxes on rooms and meals. The rooms tax was amended in July 2019 to include short-term rentals (e.g. Airbnb). The room occupancy tax is 6% and the meals tax is 0.75%. Both are collected by the state Department of Revenue (DOR) and returned to participating municipalities.

“The money flows from the local establishment — restaurant, hotel, retailer — directly to the State, who in turn distributes the funds back to the municipality on a quarterly cycle,” Carmel said.

See Edge video below of Monday’s selectboard meeting via Zoom. Fast forward to 1:12:50 for the presentation on sales tax revenues:

In 2018, voters in town meeting approved a 3% local option sales tax on cannabis sales. Theory Wellness, which had already opened a medical marijuana dispensary, launched its recreational shop in January 2019. The others followed: Rebelle in September 2020; Calyx in November 2020; and Farnsworth in March 2021.

There are two separate taxes that provide a source of cannabis revenue for municipalities that host so-called adult-use cannabis stores: a 3-percent local sales tax added to the state excise and sales taxes; and a community impact fee that is typically 3 percent of a store’s gross sales.

The latter is a point of negotiation between town and applicant as part of a host community agreement, as required by the state Cannabis Control Commission. Approximately half of the Great Barrington’s cannabis revenues were generated by the community impact fee.

The use of community impact fee revenues, however, are restricted. According to the CCC, the fee “shall be reasonably related to the costs imposed upon the municipality by the operation of the marijuana establishment.”

The rooms, meals, and cannabis sales tax revenues, on the other hand, are unrestricted. After the town receives the quarterly payments from DOR, the money goes directly into so-called “free cash,” a reserve fund that can be used to close budget gaps or limit property tax increases.

The revenues from the community impact fee, however, are supposed to be used only to mitigate the financial impacts of the stores, including increased traffic, safety, substance abuse, and the like. It is also important to note that CCC regulations specifically state that those costs to the municipalities must be publicly documented and shall not “be effective for longer than five years.”

The town has established a community impact funding committee to determine how the money is spent. The most recent grants awarded from the community impact fee went to the Railroad Street Youth Project, Construct Inc., Volunteers in Medicine, Berkshire South Community Center, and the Berkshire Hills Regional School District. For fiscal year 2022, the town is continuing to accept grant applications until August 31. Click here to see the application.

Over the last six fiscal years, the town has collected more than $1.6 million in meals taxes and in excess of $3.1 million in room occupancy taxes. The yearly totals for both declined significantly in fiscal year 2021 when the COVID-19 pandemic severely disrupted the restaurant and hospitality industries (see page 6 of Carmel’s presentation).

Interestingly, some towns, such as Northampton, have dropped the community impact fee, which the Massachusetts Cannabis Business Association has called a “legalized extortion fee” and an impediment to economically disadvantaged cannabis entrepreneurs. A writer in Commonwealth Magazine has asserted that the “3% cannabis impact fee covers costs that don’t exist.”

“After more than two years of legal cannabis sales, it’s hard to make a case that towns have incurred any such costs,” wrote James Borghesani, who served as communications director for the 2016 cannabis legalization campaign. “There have been no reported incidents of sales to minors, no reports of increased crime around cannabis stores, no reported increase in cannabis-intoxicated driving arrests, no reported impacts on nearby businesses or neighborhoods, and no reported staffing or budget increases in police, fire, or health departments attributable to cannabis stores.”

Charlotte Hanna, who owns the Rebelle cannabis shop in Great Barrington, told MassLive she applauded Northampton’s decision, and added that she thinks the move shows an “enlightened” point of view toward the cannabis industry and that she hopes other towns and cities will follow suit.

Totaling $4.14 million last year alone, the various sales taxes and cannabis community impact fee receipts are significant sources of revenues for the town of Great Barrington. The town’s operating budget for fiscal year 2022, which began on July 1, is nearly $13 million. The town’s current contribution to fund its portion of the Berkshire Hills Regional School District is approximately $18.5 million.

The cultivation, sale, and use of recreational cannabis-related products was legalized in Massachusetts through a 2016 ballot initiative. The measure passed by almost 7.5 percentage points statewide, by almost 30 points in Great Barrington and by almost 24 points in Sheffield. Implementation of the new law was left to the hastily created state Cannabis Control Commission. Preceding that law, medical marijuana was legalized in Massachusetts in 2012 through the same process.