Members of the Federal Reserve Bank recently attended the annual Economic Policy Symposium in Jackson Hole, Wyo. Also known more plainly as the “Jackson Hole meeting,” it is where global central bankers, economists, and policymakers discuss major economic issues. It is a high-profile conference and is often a platform for the Federal Reserve chairman to hint at future moves in monetary policy.

There was a lot in Federal Reserve Chair Jerome Powell’s speech, which is transcribed on the Federal Reserve’s website. One of the most telling lines from the speech was when Powell said, “With policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.”

Much of what Powell said signaled that an interest rate cut is likely to come at the Fed’s September 17, 2025, meeting. President Donald Trump is likely pleased about that, as he has been pressuring the Fed to cut rates.

It isn’t just Powell’s comments that point to lowered interest rates. Both politics and policy suggest several more rate cuts in 2026.

The Federal Funds Rate, which is essentially the overnight rate that banks pay to borrow money, is determined by a vote by the Federal Open Market Committee (FOMC). That rate is one factor that influences other rates, such as the prime rate or mortgage rates.

As stated, the president wants the Fed to cut rates, presumably to lower the rates at which corporations and households borrow and to, in turn, stimulate the economy ahead of the November 3, 2026, elections. Which, in turn, could help win more Republican seats, allowing the president to continue his policies. Many people would agree that tracks with previous presidents’ game plans.

There are 12 voting members of the FOMC. Four of them are Reserve Bank presidents who serve one-year terms on a rotating basis. The other eight include the president of the Federal Reserve Bank of New York, the chairman of the Fed, and six other Fed governors.

Those “other eight” can be the most influential in the voting process. There is Chair Jerome Powell, whom President Trump is expected to remove in May 2026. And there is Stephen Miran, whom President Trump recently nominated to fill the vacant seat left by Adriana Kugler. Two other governors, Michelle Bowman and Christopher Waller, have echoed President Trump’s narratives.

More recently, the Federal Housing Finance Agency (FHFA) has entered the conversation. If you go to the FHFA website, President Trump is notably front and center on their website, for whatever that is worth—if anything. FHFA Director Bill Pulte announced that he is referring Fed Governor Lisa Cook to the Department of Justice, alleging mortgage fraud.

Then there is Fed Governor Lisa Cook, whom President Trump is attempting to fire from her position on the FOMC after FHFA Director Bill Pulte announced that he is referring her to the Department of Justice, alleging mortgage fraud. I don’t want to get into those details, but Cook apparently did not notify a mortgage lender about a change in residence. As a result, two homes were listed as primary on mortgage documents, which was a violation of a mortgage covenant.

Yes, that is absolutely a bad thing. A Fed governor should be held to a higher standard. For perspective, however, a 2023 study by the Philadelphia Fed found that around three percent of all new mortgages originated to the same purchaser of the primary home for another home within one year. That would equate to tens of thousands of loans per year. Was it just stupid? Or was it fraud? Does anyone care? I suspect Pulte and Trump do not care, other than it being a possible way to remove her for alleged cause then replace her with another voting member who is more likely to follow President Trump’s desired direction of interest rates.

That would mean the new Fed chair, Cook’s replacement, Miran, Waller, and Bowman would be pushing for interest rate cuts. That is five of the eight governors.

Now, remember, there is a simple 55-year-old tried-and-true investment saying: “Don’t fight the Fed.” Martin Zweig, a renowned investor and market forecaster, coined that term in 1970. The Fed’s monetary policy is typically a significant factor in determining the direction of the stock market. In other words, if the Fed cuts interest rates, the lower borrowing costs should stimulate the economy, improve corporate earnings, and lift stock prices.

So what happens to the stock market when the Fed cuts rates? The Fed’s last rate cut was on December 18, 2024. It cut rates by one percentage point from September to December.

Let’s assume the Fed will cut rates at its September 2025 meeting. I don’t think they should, but it is not an unreasonable expectation, given that the futures market indicates a better than nine-in-10 chance of a cut at that meeting. (It was seven in 10 before the Jackson Hole speech by Powell.)

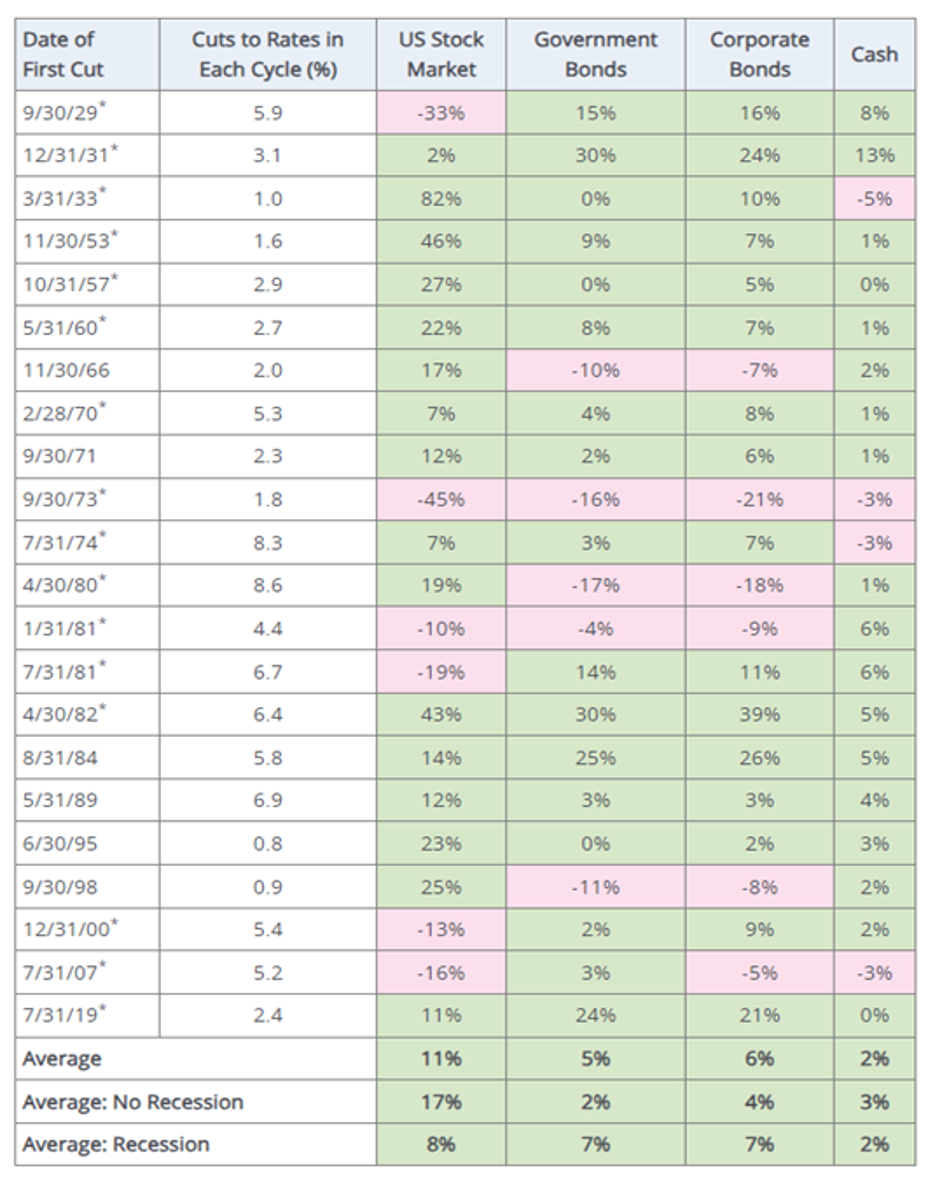

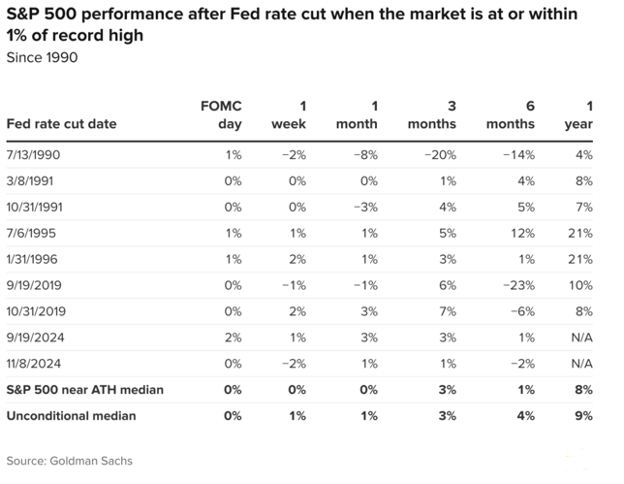

Will this be the start of a new rate-cutting cycle? Or the continuation of the one that began in September 2024? An argument can be made either way, but let’s say it is a new one. Looking back on nearly 100 years of history, you can see how the stock market performed 12 months after the first rate cut. The average return 12 months after the first cut in all rate-cutting cycles was 11 percent, according to the Hartford Funds. That is about average for a yearly gain—not bad at all. However, let’s also consider that some of those rate cuts were in response to a recession, when stock prices could have been dropping, and thus dragged down the average return. In the 12 months following the first rate cut of a cycle when there was no recession, the average return was 17 percent. Could it be different this time? Of course. In particular, you may be wondering what happens to stocks after a rate cut if the market is trading at or near its highs, as it is now. Of course, between now and an assumed rate cut in September 2025, the stock market could be significantly lower, which might make that concern moot. But let’s explore it now in case we need to consider it later. Going back to 1990, there have been nine occurrences when the Fed cut interest rates while the S&P 500 was trading within one percent of a record high.

Could it be different this time? Of course. In particular, you may be wondering what happens to stocks after a rate cut if the market is trading at or near its highs, as it is now. Of course, between now and an assumed rate cut in September 2025, the stock market could be significantly lower, which might make that concern moot. But let’s explore it now in case we need to consider it later. Going back to 1990, there have been nine occurrences when the Fed cut interest rates while the S&P 500 was trading within one percent of a record high.

The 12-month return after those cuts averaged eight percent. While that is much less impressive than the 17 percent average return under the aforementioned conditions, it is still in line with historical averages. That would be good, especially given the lofty valuations of the stock market.

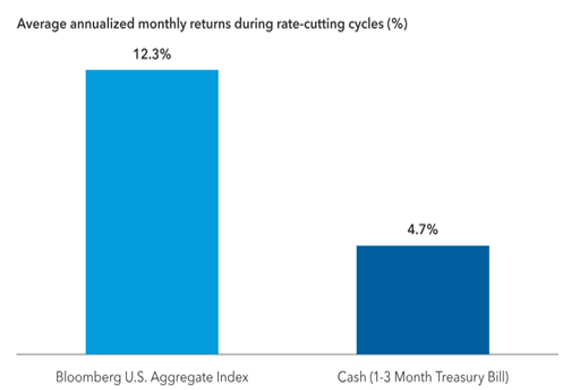

The Capital Group noted that positive returns were not limited to the stock market.

Bonds also performed positively after the start of an interest rate-cutting cycle over the last 30 years.

Now, there is another saying: “Lies, Damn Lies, and Statistics.” We can all cherry-pick data over time and use different definitions to manipulate it and tell the story we are looking to tell; however, no matter how much I tortured the data, rate cuts during periods of economic expansion tend to coincide with stronger returns. Although the first half of 2025 averaged out to be weak and worrisome for the economy, the odds favor an expansion rather than a recession. Even as an investor who has always looking for the exit door to keep what I have, I am inclined to stay in the market for now.

Allen Harris is an owner of Berkshire Money Management in Great Barrington and Dalton, managing more than $1 billion of investments. Unless specifically identified as original research or data gathering, some or all of the data cited is attributable to third-party sources. Unless stated otherwise, any mention of specific securities or investments is for illustrative purposes only. Advisor’s clients may or may not hold the securities discussed in their portfolios. Advisor makes no representation that any of the securities discussed have been or will be profitable. Full disclosures here. Direct inquiries to Allen at AHarris@BerkshireMM.com.